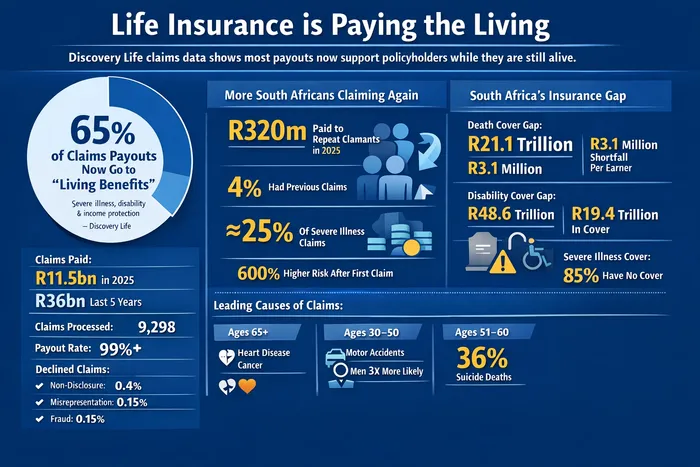

South Africans are increasingly claiming insurance benefits while they are still alive. According to Discovery Life, about 65% of its claims payouts now go towards “living benefits”.

Image: File photo.

South Africans are increasingly claiming insurance benefits while they are still alive. According to Discovery Life, about 65% of its claims payouts now go towards “living benefits”.

The shift towards severe illness cover, disability benefits and income protection is significant when compared with the death-claim-weighted payouts of previous years.

Discovery Life paid out R11.5 billion in claims in 2025, part of R36 billion over the past five years. The insurer processed 9,298 claims last year at a payout rate of more than 99%. Claims were declined in a small number of cases: non-disclosure accounted for 0.4% of rejections, misrepresentation for 0.15%, and fraud at 0.15%.

“Trying to break that narrative that life insurance is for death is very important,” says Kashmeera Kanji, head of Distribution Strategy and Market Analytics at Discovery Life. “We see claims across all ages; death is not just an old age thing. It happens across the board.”

Claiming more than once

One of the clearest shifts in claims patterns is the rise of policyholders claiming more than once. As medical treatment improves, more people are surviving serious health events such as heart attacks, strokes and cancer – but those same individuals may face further complications later.

“People who survive a severe illness are more likely to experience another medical event,” says Discovery Life deputy CEO Gareth Friedlander. “That’s purely because medicine is really good at life.”

Discovery reveals insurance statistics from 2025.

Image: ChatGPT

In 2025, Discovery paid R320 million to multiple claimants. Clients who had submitted a severe illness claim before 2025 made up 4% of its risk pool but accounted for nearly a quarter of all severe illness claims last year.

The probability of claiming again after a first claim is almost 600% higher than average, says Friedlander. “You can see some clients on their third claim, their fourth or more claim. We’ve had a single client with 21 claims on one policy. We’re seeing more and more prevalence of people claiming multiple times,” he says.

Friedlander adds that this highlights the importance of insurance. “When you’re talking about massive heart attacks and strokes and cancer journeys and these attacks that a severe illness has on a family, you can kind of get a sense of how under underinsured” South Africans are,” he adds.

The underinsurance gap

South Africa has a significant life and critical illness insurance gap. The Association for Savings and Investment South Africa (ASISA) calculates that if households wanted to maintain their standard of living after what it terms a “death event,” the collective shortfall amounts to R21.1 trillion – or R3.1 million for the average earner.

The disability gap is larger still. Maintaining living standards after a disability event would require R48.6 trillion in cover nationally, against actual cover in force of R19.4 trillion. Severe illness cover is the most neglected of all. ASISA data shows 85% of South African earners have none.

An average South African earner needs to have around R2.1 million to ensure that his or her family can maintain their standard of living – and there’s an average death insurance gap of about R1.3 million.

In the case of a disability event, the average South African would need to provide for R3 million in cover, and ASISA says there’s an average gap of about R1.8 million.

Who is claiming, and why

Discovery’s data shows heart and artery disease and cancer are the leading causes of claims for those aged 65 and older. For the 30 to 50 age group, motor vehicle accidents are the most common cause of unnatural death. Men are three times more likely than women to die in a fatal motor vehicle accident, according to Discovery’s five-year figures.

Among those aged 51 to 60, suicide accounts for 36% of unnatural deaths. The overall rate has declined – from 35% to 27% - which Discovery attributes partly to mental health interventions including cost-free counselling programmes.

“Suicide rates have come down from last year. It’s moved in the right direction, but still at a level where we’re concerned,” says Sylvia Steyn, head of Claims and Service at Discovery Life.

What consumers want

The living benefits shift is also consumer-driven. The Capgemini World Life Insurance Report 2026, conducted jointly with the Life Insurance Marketing and Research Association, found that while 68% of adults under 40 see life insurance as essential for a healthy financial future, current offerings do not align with their financial priorities, hindering adoption.

Younger consumers cite a misalignment with their current stage in life, high premium costs, and lack of immediate benefits as the main barriers to purchasing, says the Capgemini report.

People under the age of 40 want living benefits that provide financial flexibility around life events, support for wellness, and aid during a critical illness, says Capgemini.

Global life insurance premiums are forecast to grow at just 0.9% compound annually through 2040 Insurtechdigital, according to the same report, reflecting the scale of the industry’s challenge in remaining relevant to the next generation of policyholders.

This aligns with Discovery’s shared-value model, which rewards policyholders for healthier and more financially responsible behaviour through lower premiums, cashbacks and product discounts. In 2025, Discovery paid R1.25 billion in PayBacks and R1.16 billion in Cash Conversion benefits – money paid to clients who are alive and engaged, not claiming a death benefit.

The longest duration of a Discovery policy before a death claim was nearly 25 years. The shortest was 29 days.

PERSONAL FINANCE