Overdue balances dropped by R3 billion in the third quarter, bringing the total overdue amount to R212 billion.

Image: Pexels

South Africans are carrying a debt load of about R2.6 trillion, which works out to roughly R43 000 for every man, woman, and child.

Yet, for the first time in a while, households are falling behind slightly less.

This is according to the Eighty20 Credit Stress Report, compiled with XDS, for the third quarter of 2025.

Overdue balances dropped by R3 billion in the quarter, bringing the total overdue amount to R212 billion.

The number of loans in arrears fell by almost 90 000, pulling the share of overdue loans down to 33.1%, the lowest point since early 2023.

At the same time, one million more loans were paid on time, continuing a seven-quarter streak of improvement.

That means just over 8% of all debt is now past due, down from 8.3% in the previous quarter. Most of the improvement came from people catching up on personal loans and vehicle finance instalments.

The employed lower-middle-income group – mostly women with store accounts and sometimes credit cards – now numbers 8.6 million people.

They took out more than 2.1 million new loans in the quarter, most of them retail and personal loans.

This group owes R113 billion in total, about R13 000 per credit-active person.

Overdue balances climbed 6% from last year, and just over half of the group is still in default. However, this is an improvement from last year, with defaults down 7% in relative terms.

The 4.1 million middle-income earners with families, mortgages and frequent shopping routines held 12.9 million loans this quarter.

They took up 1.2 million new loans, with personal loans making up nearly three-quarters of the total.

Their total debt has risen to R541 billion, around R130 000 per person.

Overdue balances rose 5.5% year-on-year, but fewer people in the segment are defaulting. The share of those with at least one loan in default fell to 41.5%.

South Africa’s wealthiest 5% – the Heavy Hitters – continue to grow their borrowing faster than other groups.

There are now 2.2 million credit-active individuals in this segment, up 4% from last year.

They took out 693 000 loans this quarter, including 91 000 vehicle finance agreements.

That means this small group accounted for nearly two-thirds of all new car and asset finance loans.

Their home-loan balances climbed to R1 trillion, which is more than seven times the total debt load of the Middle Class Workers.

South Africans are buying cars again – or at least financing them more aggressively. New vehicle asset finance loans rose to 139 000 this quarter, the highest in five years.

Loan terms are also getting longer. Nearly 16% of new car loans now stretch beyond seven-and-a-half years, compared to 12% a year ago.

Longer terms usually mean lower monthly payments, suggesting lenders are helping consumers manage stretched budgets.

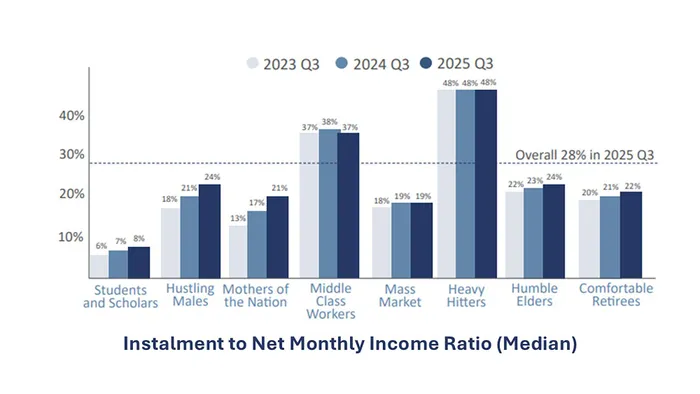

South Africans are paying, on average, 28c for R1 brought home on debt.

Image: Eighty20 & XDS

The total number of credit-active consumers grew almost 4% over the year.

While overdue balances climbed 9%, fewer people have fallen three months or more behind on payments.

The share of consumers with at least one serious default dropped to 40.4%, continuing an improvement seen since late 2023.

Default levels are lowest among Heavy Hitters, Humble Elders and Comfortable Retirees. The Mass Market remains most vulnerable, with 51% in default.

On average, South Africans spent 28% of take-home pay on loan repayments in quarter three. For every R10 earned, almost R3 went straight to banks.

Heavy Hitters spent the most – nearly half of their income.

Middle Class Workers committed just over a third.

The Mass Market spent 19%, while Comfortable Retirees used 22% of their income on servicing debt, up from 20% a year ago.

The net result is that consumer credit markets expanded, with more active accounts and larger balances across most categories. Vehicle finance was particularly strong, reaching the highest levels in three years.

IOL BUSINESS