Looking ahead: Can economic and market strength repeat in 2026?

US growth continues to lead the charge, with the initial estimate for the third quarter 2025 coming in at a very strong 4.3%, well above trend growth, says the author.

Image: The Washington Post

Global growth continued to improve throughout 2025, with the latest reading of 3.4% according to the Bloomberg economics global GDP tracker. US growth continues to lead the charge, with the initial estimate for the third quarter 2025 coming in at a very strong 4.3%, well above trend growth. The Atlanta Fed GDPNow forecast for the fourth quarter has deteriorated to a still very strong 3%. Trump’s One Big Beautiful Bill should continue to support US GDP into 2026, particularly in the first half as tax refunds will support both consumers and businesses.

Other developed economies are also expected to be strong in 2026 as fiscal stimulus and rate cuts flow through to the underlying economy. Europe’s defence spending kicks into gear in 2026 but really comes in from 2027 onwards, but this should be enough to boost European growth, especially after significant rate cuts and stable inflation. Japan’s new Prime Minister has also pledged significant fiscal spending in 2026 which should support the economy, even as the Bank of Japan is set to hike to rein in inflation. Australia is also continuing to grow at or above trend, with inflation remaining sticky, causing bond markets to price in the potential for the Reserve Bank of Australia to start hiking in 2026. The global economy therefore looks to see growth remain strong, but with inflation remaining sticky throughout the year.

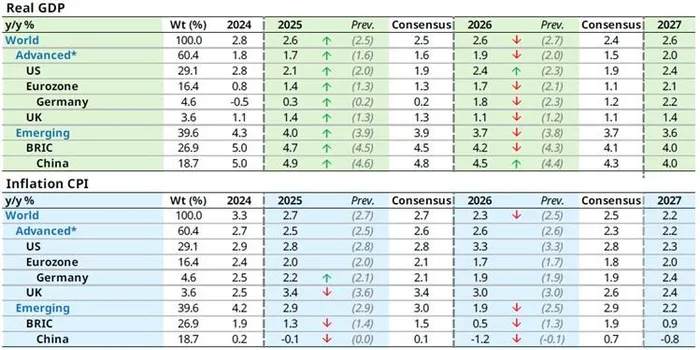

Schroders Economics Group growth forecasts are above consensus for 2026

Image: Source: Schroders Economics Group, LSEG Datastream.

US employment growth recovers

One of the main concerns from the market was that recent weakness in hiring in the US could derail this positive growth story. Non-farm payrolls collapsed after the April ‘Liberation Day’ tariff announcement, as corporates waited for more clarity on what Trump’s Trade War 2.0 meant for them. It has been hard to distinguish between corporates entering a wait-and-see mode, versus those who had to cut jobs given the potential weakening of margins as import prices rose.

October saw a large reduction in Federal workers as Elon Musk’s ‘DOGE’ cuts came through, but private hiring is showing signs of recovery. When looking at the 3-month average change in private payrolls over the year, it has followed the same trajectory as we saw in 2024, where we also had an employment scare. Hopefully we continue to follow a similar path to growth as the year rounds out. While unemployment did rise over the year to 4.56% in November, this was mainly from an increase in participation rate. Continuing jobless claims remains in line with recent averages.

All eyes on the Federal Reserve

Inflation came in below expectations in December at 2.7% versus expectations of 3.1%. But just like the employment data, it’s hard to know how accurate this is given the government shutdown prevented works from collecting accurate information. Despite this inflation surprise to the downside, bond markets have not priced in a cut during the January meeting. The Federal Reserve (Fed) will likely put far more weight on the December data figures once they come out.

In the meantime, the bond market is pricing in two cuts for 2026. As Jerome Powell’s term ends in 2026, Trump has been hinting at his preferred candidates to replace Powell. Given his inclination, he is pushing for a more dovish Fed chair, who he hopes will likely cut rates to “below 1%”. While this is very unlikely to occur given the strength of the economy and still elevated level of inflation, it shows there is a risk of losing central bank independence and a likely more accommodative Fed.

We continue to believe the US economy will be strong next year, with rate cuts and fiscal stimulus keeping demand buoyed. The consumer continues to remain employed, receive positive real wage growth and will continue spending into 2026. Corporate activity will likely also pick up after a soft patch post Liberation Day. Globally, rate cuts and an increase in fiscal stimulus should see global growth improve into 2026 as well. We therefore remain positive on the global economy overall into 2026.

Sebastian Mullins, Head of Multi-Asset and Fixed Income, Schroders Australia

Image: Supplied

Sebastian Mullins, Head of Multi-Asset and Fixed Income, Schroders Australia

*** The views expressed here do not necessarily represent those of Independent Media or IOL.

BUSINESS REPORT